Last Updated :

July 9, 2026

Home InsuranceHome Warranty vs. Homeowners Insurance: What’s the Difference?

Homeowners insurance and home warranties cover very different things. Learn what each protects, what lenders require, and when you may need both.

Home what? Homeowners often confuse these two similar sounding home protection policies, especially at closing when both come up at the same time.

But here’s the thing; They cover completely different items, and mixing them up can leave you paying out of pocket for something you thought was covered.

Here’s what each one actually does.

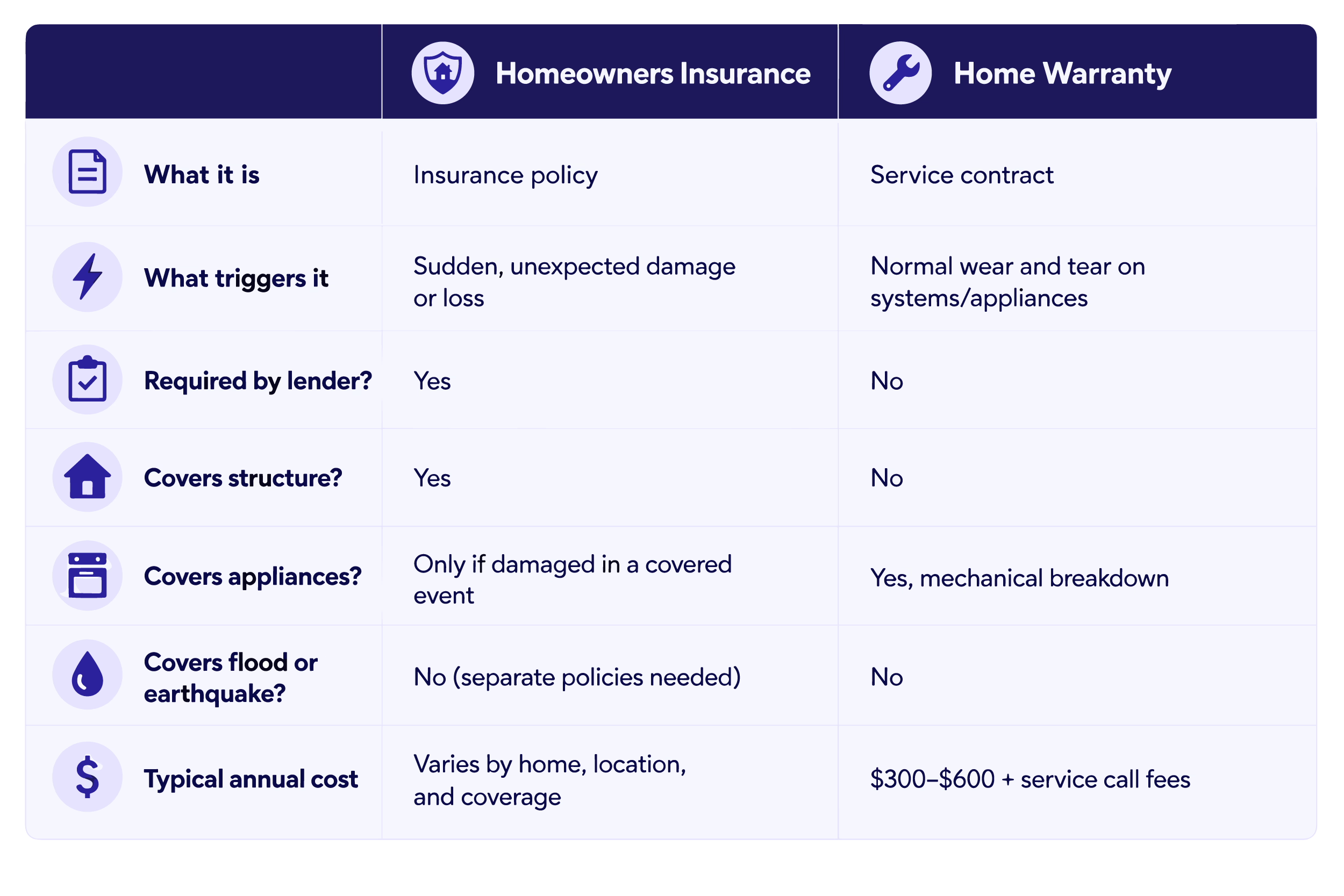

What Homeowners Insurance Covers

Homeowners insurance is an essential component of your monthly mortgage payment, and protects you against sudden, unexpected losses: fire, theft, windstorm, lightning, or someone getting injured on your property. It does not cover appliances wearing out or your HVAC dying of old age.

According to the Insurance Information Institute, a standard homeowners policy covers four things:

- The structure of your home – repairs or rebuilds if damaged by a covered event

- Your personal belongings – typically 50–70% of your structure coverage amount

- Liability protection – covers legal costs if someone is injured on your property

- Additional living expenses – living expenses like hotels if a covered loss makes your home temporarily unlivable

Mortgage lenders typically require homeowners insurance as a condition of your loan. It is not usually optional.

There are some exceptions to homeowners insurance you should be aware of. Standard policies generally do not cover flood damage, earthquake damage, mold, pest infestations, or normal wear and tear. That last one is where a home warranty fits in.

What Is a Home Warranty and What Does it Cover?

A home warranty is a service contract, not an insurance policy. It may cover some repairs or replacement costs when home systems and appliances break down from normal use over time.

A typical plan covers:

- HVAC systems (heating and air conditioning)

- Plumbing and electrical systems

- Major appliances: refrigerator, dishwasher, washer/dryer, oven

- Water heater

When something breaks, you call the warranty company, pay a service call fee, and a technician is dispatched. Annual plans fluctuate in cost depending on what is covered and the area you live in - but its important to remember that this is completely separate from your home insurance policy.

What a home warranty does not cover: pre-existing conditions, improper maintenance, structural damage, or anything caused by a sudden event like a storm or fire. Those belong to your insurance policy.

Side by Side

Do You Need Both?

That’s up for you to decided. But remember, Home Insurance is required by your lender and is an essential component of keeping your home protected. A home warranty can be helpful in some instances, but does not provide the same safety net that an insurance policy does. These two products do not overlap, they complement each other.

Your homeowners insurance will not pay when your 12-year-old furnace stops working in January. That’s wear and tear, not a covered event. Likewise, your home warranty will not help when a tree falls through your roof. That’s what insurance is for.

A home warranty may be worth considering if your home has older systems and appliances, or if you want more predictable repair costs in the first few years of ownership. It is not a replacement for insurance, and it will not satisfy your lender.

To Summarize

Homeowners insurance covers sudden, unexpected losses. A home warranty covers the everyday breakdown of systems and appliances over time. You need insurance if you have a loan. A warranty is a personal, non-required decision, based on your home’s age and your tolerance for repair surprises.

Not sure if your homeowners insurance is keeping pace? Compare quotes in minutes and make sure you’re not overpaying or underprotected.

.svg)

.svg)